June 16, 2015 •Brian Watson

With patients asked to shoulder a larger portion of healthcare costs, providers are looking for ways to improve how they communicate with consumers about financial responsibilities

With patients asked to shoulder a larger portion of healthcare costs, providers are looking for ways to improve how they communicate with consumers about financial responsibilities

Many hospitals and health organizations have already spent a considerable time and resources in the pursuit of smarter statement design, only to have patients still struggle to consistently understand the financial side of their care.

While statement improvement is a good start – one with clear financial benefits – more needs to be done to improve how patients anticipate and manage costs.

A recent TransUnion study underscores the challenge. Of the insured patients surveyed, 54% reported that they were either sometimes or always confused by the healthcare bills they receive. And 62% were similarly confused when it came to what costs they were required to pay out-of-pocket

Part of that can be traced back to traditional revenue cycle stumbling blocks, such as statements that aren’t simple, clear, and easy-to-understand.

But another contributing factor – one that’s increasingly important in today’s high-deductible marketplace – is that many consumers don’t have a strong grasp of what their insurance plan actually covers. Or the extent to which they’re personally responsible for out-of-pocket costs.

Statement clarity is critical. But even a statement that follows patient friendly guidelines will struggle to communicate with patients that lack a solid grasp of what exactly their insurance plan covers, or what they’re being asked to pay out-of-pocket – and why.

The Knowledge Gap

A 2013 experiment from Carnegie-Mellon healthcare economist George Loewenstein illustrates the often wide gap between what people think they know about insurance and what they actually do.

In the survey, Loewenstein asked 202 people with employee-sponsored health coverage to define four basic insurance concepts – deductible, copay, coinsurance, and maximum out-of-pocket – using provided multiple choice answers.

Over 90% of participants were confident they understood the meaning of each of the four terms. But while most could correctly answer one or two questions (78% know what a deductible was, 72% copay, 34% coinsurance, and 55% maximum out-of-pocket), only 14% got all four correct.

The survey then presented respondents with a hypothetical insurance plan and asked them to figure out what a four-day hospital stay would cost. On this exercise, only 11% came up with the right number – and just 14% were within $1,000 of the answer.

Those results shouldn’t come as a surprise to most patient financial professionals.

After all, as Lowenstein told the Washington Post, "I have a PhD in economics and I've spent a bunch of time giving insurance companies feedback about policies, and I still find them difficult to understand”.

Self-Pay Rising

Between Medicaid expansion and state and federal insurance exchanges, an estimated 16.9 million Americans have been newly insured under the Affordable Care Act as of February, 2015 – including many with coverage for the first time. But while more Americans are gaining coverage, patients are by no means shielded from out-of-pocket costs

As employers embrace cost-sharing measures and more consumers gain coverage through health insurance exchanges, patients face higher premiums, more out-of-pocket costs, and increased discretionary spending on non-covered health and wellness services.

For example, the portion of workers covered by plans with a general annual deductible of over $1,000 has increased from 10% in 2006 to 41% in 2014. And almost half of large employers offer a high-deductible, consumer-directed health plan (CDHP) option – up from 39% in 2013.

Additionally, nearly 90% of patients enrolled in coverage via health insurance exchanges have selected Silver, Bronze, or Catastrophic plans with higher deductibles, co-payments, and out-of-pocket maximums.

That change will likely affect collection costs and profit margins.

Self-pay is typically more expensive, more time consuming, and requires more hands-on attention than reimbursements from a payer. Nearly half of patients wait more than a month to pay an outstanding balance. On average, providers send 3.3 statements before payment. And, without contracts, there’s no assurance that you’ll receive a certain payment within a set time.

Reducing Stress on Revenue Cycle Ops

With businesses embracing cost-sharing measures and more Americans using insurance exchanges to receive coverage, the move from private and public insurance to direct patient payment looks like a long-term trend.

Today, patients with employer-provided insurance face higher premiums and deductibles. And those that use state and federal marketplaces are overwhelmingly choosing high-deductible options.

That's what makes both the Loewenstein study and the TransUnion survey mentioned above so important.

Many patients are already struggling to understand their statements. They’re often uncertain what they owe out of pocket and what’s been paid by insurance. What’s more, most of those patients have been have been covered by insurance for years.

And they’re soon to be joined by millions of consumers that have little or no history of using insurance to pay for healthcare.

But the problem isn’t confined to confusing statements or lack of knowledge of key insurance concepts. It’s a bigger picture issue: most patients are only now starting to become active healthcare consumers. Spurred by higher deductibles or change in coverage status, they’re starting to behave like shoppers: asking questions about cost, weighing quality, or deciding if a service is necessary.

In the long run, that’s a good thing. Patients will not only be able to anticipate out-of-pocket costs, they’ll also be less likely to delay or skip preventive care out of concern for an unknown cost. But getting there is a challenge – one that, in the near-term at least, could shrink margins, increase collection costs, and threaten already tight budgets.

In the rest of this post, I’ll outline twelve steps providers can take to lessen the short-run burden by helping patients better understand their financial responsibility.

More Transparency

As patients transition from passive to active healthcare consumers, they are increasingly reliant on providers for help anticipating and managing the costs of treatment.

Making sense of the complicated way health services are paid for is extremely difficult for patients to handle alone. While charge data is often easily accessible, patients lack the kind of meaningful price information to forecast out-of-pocket costs, make apples-to-apples comparisons about care, and budget for elective and preventative services.

Being transparent and proactive in communicating cost and quality information with patients is among the best ways for providers to bridge the knowledge gap that patients have about financial responsibility.

A patient that understands what they’ll owe out-of-pocket – even if it’s just a ballpark estimate – will be better prepared to deal with the financial fallout from care. That eliminates sticker-shock, enables you to better indentify patients that need additional financial outreach, and clearly signals your concern for patients – both physically and financially.

• Provide accurate pre-service financial estimates. By integrating eligibility information with payer contracts and historical payment data, you can serve personalized patient estimates that frame payment expectations and set the stage for further pre-treatment financial counseling and support.

• Assess propensity to pay. Categorizing patients based upon financial profile can help identify patients that meet state and federal financial aid guidelines. And, for patients with the ability to pay, it can provide grouping for more targeted financial activities.

• Consider using a pre-service estimate letter. This helps proactively educate patients about their financial responsibility. Best-practice examples not only provide a specific price for an upcoming service, but also define commonly used billing terms – deducible, coinsurance, copayment – and offer an easy-to-understand explanation of how the amount due figure was reached.

Simpler Statements

In a best case scenario, patients will have a good idea of what they’ll be asked to pay out of pocket before they receive a statement.

But organizations that provide clear, simple, and intentional financial correspondence can help patients better understand what they owe – even without an estimate in hand or strong grasp of common insurance terms.

To be successful, patient financial communication must be actionable. And the key is clarity.

There’s a common tendency to want to add more and more information to billing documents to ensure that nothing falls between the cracks. But a narrow focus on the core message can help patients prioritize what really matters – your charges, what’s been paid already (out-of-pocket or through insurance), and what they now owe.

To strip a financial document to the core message, you need to prioritize exclusion.

• Embrace clean design. Plenty of white space helps keep patients from getting overwhelmed and makes it easy for them to focus on key billing details.

• Edit, edit, edit. Eliminate all unnecessary information. An account summary, payment channels, and customer service contact information is all critical. That picture of your facility might look nice, but does it really increase the functionality of the statement?

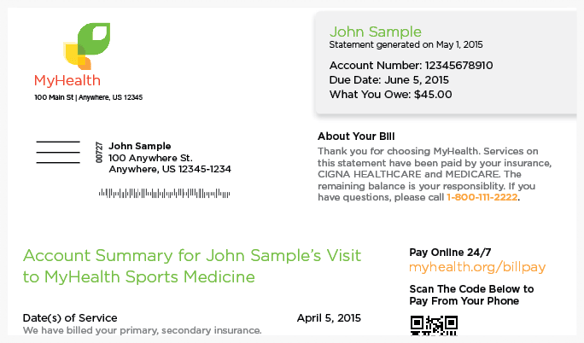

• Use "bite-sized"instructions to aid understanding. Adding clarity without increasing statement clutter can be tricky. Consider using a brief "About Your Bill" message above the fold on your statement to frame patient expectations. As in the example below, this can used to let patients know that their insurance has been billed and all charges on the statement are now their responsibility to pay.

Placing billing instructions above the fold on the first page of your statement can help frame patient expectations.

• Consider a snapshot "resource summary". Once again, the key is for information to be easy to understand, actionable, and related to the core goal – payment. A snapshot "resource summary" provides everything a patient needs to take action on billing cues – payment channels, billing support, and your financial assistance policy – all in one convenient spot.

Use a snapshot "resource summary" to quickly communicate important information about your payment options and financial assistance policy.

• Use default design. Some patients will want to view an itemized bill. But that’s likely a small number. And sending everyone a statement that is itemized will increase page count and on-bill clutter. Make the simple option the default choice. If a patient wants an itemized bill, provide an option to view one via an online billing portal.

• And simple language. Jargon is an enemy of simplicity. So strike all billing jargon, insurance terms, and medial codes from your statements in favor of plan, simple language.

More Technology

As consumerism continues to take hold, healthcare providers will have the challenge of meeting consumer expectations set by other retail and service business. And technology is set to play a key role.

Most consumers are used to self-service payment and on-demand outreach – such as text messages or email updates. By integrating high-tech solutions, healthcare organizations can better meet the cost and productivity challenges associated with serving patients with a self-pay balance after insurance.

• Make billing and payment resources available on your website. That includes frequently asked questions, commonly accepted insurance, estimation tools, and your financial assistance policy.

• Provide multiple payment options. Seventy percent of bills are paid using electronic channels. And 40% of smartphone users have paid a bill from their phone. Meet patients’ payment needs by offering multiple channels – both traditional and tech-supported options, like online, mobile, point-of-service kiosks and tablets, and automated IVR.

• Use mobile outreach. Ninety percent of Americans own a mobile phone – nearly two thirds of which are smartphones. Tap into that captive audience to deliver SMS text message and IVR pre-service estimates and post-discharge payment reminders.